Since the 2006 publication, by Bantam Press, of Richard Dawkins The God Delusion many commentators have critiqued it, largely for being an evangelical atheistic attack on religiosityand the mystical mind: The problem, for most commentators, seems to be the evangelical nature of Dawkins’s attack itself rather than the content of his argument. Indeed, I see more attacks on his style than I do on his argument.

My contention is that Dawkins makes a categorical error in trying to apply the scientific method of the natural sciences to disprove an entirely logical phenomenon. In terms of logic I shall now attempt to disprove his theses, and to demonstrate that God does indeed exist.

Dawkins is a natural scientist. His method of reasoning is firmly rooted in 20th century scientific positivism. Prior to Karl Popper’s Logic of Scientific Discovery (1959), it was assumed that a scientific proposition could only be maintained if it accorded to establishedfact. Popper pointed out that no theory could be maintained if it is refuted by some data of experience. Popper was contrasting say a mathematical proof, which is entirely in the mind (such as 2 + 2 = 4) which needs no empirical testing to prove it, with for example the fact that water will boil at a certain temperature, which needs to be empirically expressed before one believes it. The next step in the process is to declare a theory “un-scientific” if it cannot be refuted by experience. This is reasoning a posteriori dependant on experience. In applying scientific method to the question “does God exist,” the answer from Dawkins is a resounding NO!

If these are the rules of the game, then we can only but agree with him. Only the data of experience will now prove to Dawkins that God exists. As we have none that seems credible, it is a matter of Faith. Faith v Science, for the Modern Mind, places most reasoning people in the camp of Science. The un-reasoning mind is therefore deemed to be the religious and mystical mind and somewhat prejudiced and backward and or primitive. Dawkins, in the name of science and what he understands as reason, proceeds to demolish some of the more wildly mystical and witch doctor interpretations and commands of religion with some aplomb. Fair play to the man for sure as they deserve to be savagely attacked by an acute mind such as his.

However, as man can introspect as say a chemical or a stone, a gene or any subject of the natural science can not, we have open to us another method of acquiring knowledge, that is via reason independent of experience i.e. knowledge derived a-priori. It should also be noted at this point, that for a thoughtful introspecting human, being capable of making abstract deductions, experience is history and nothing else. It cannot tell us anything but past history, past data series. It can yield up no irrefutable truth, just very good associations, correlations etc. In fact as Dawkins points out, Darwin’s Theory of Evolution is very highly probable to be true, but it has the possibility of being refuted by other experience. As such Darwinian Theory is scientific, but we cannot say for sure, for 100% certainly, that it is true. Whilst Evolution has mounds of scientific data to support it, lots of experience, lots of history, God does not. As Dawkins admits, this does not kill God off stone dead; it just makes God very, very highly improbable whereas something like Evolution, very, very highly probable. I would disagree with Dawkins on this point, God as a scientific proposition is not a conjecture that is capable of being refuted: God is not open to proving or disapproving via experience.

Indeed we have open to us introspecting beings the beauty of knowledge acquired a-priori. Subjects of the natural scientist are denied this; the subject of the Human science is not. God exists via the realm of the a-priori, independent of experience, and can never exist in the realm of the a posteriori; by the data of experience or history.

What is a-priori correct reasoning? How do you correctly reason?

Aristotle worked out that there were three Laws of Logic the formal explanation is as follows:

- A=A: The Law of Identity. A table is a table because it just is so.

- Not (A and not A): The Law of Non-Contradiction, if I am being boring, then it is not the case that this talk is not boring

- A or not A: The Law of the Excluded Middle, if you have two contradictory properties i.e. green and not green, all things are either one of the two, green or not green, and certainly not both.

Any argument that contradicts the above needs to be discarded.

A great example of how you can use logic to reason correctly is in maths. For example, we all know that if 2 x X = 20, X must be 10; if you tried to argue it any other way, you would conflict with the Laws of Logic. However, any which way you turn around the equation, with a logical argument, will always lead to a truthful answer, as the premise is correct.

This is very powerful because we can establish truthful propositions in logic that can only be refuted should their premise or the deductions from them fall foul of one of Aristotle’s a-priori laws of logic. Not only are the truths of mathematics rooted on the a-priori, so are the truths of the human sciences. For example; the Austrian polymath Ludwig Von Mises shows in his masterful book Human Action (1949) how all the laws of economics can be deduced from the axiom that humans act purposefully. As Mises shows, in order to be, we act purposefully. Not being, we would not act, indeed we would not exist. We act upon satisfying our most urgent needs first, then our second most urgent needs, and so on a so forth. Ranking preferences, with the most urgent needs/demands being satisfied first, the least urgent, the furthest away in time. From this hierarchy we derive the law of demand, the downward sloping demand curve, the law of diminishing marginal utility (see here for a good illustration) and on and on it goes. Lord Lionel Robbins in the masterful 1932 book, TheNature and Significance of Economic Science shows in very clear terms how all the laws of Economics are derived from the a-priori thought process. No data of experience is needed to establish that a demand curve is always downward sloping. This has real meaning in life and imparts upon how man acts in society. Experience cannot refute these laws although many modern economists will produce sets of statistical data that seem to contradict some of the Laws of Economics, but in reality, they have just got whatever they are trying to correlate wrong. A-priori knowledge contains real truths that are not just meaningless tautologies.

To try to refute it, you cannot, as you act purposefully to do so. Just as Pythagoras’s Theorem is implied in the concept of a right angle triangle-and we knew about the concept of the right angle triangle before Pythagoras “discovered” his Theorem, so, to do the laws of economics flow from the one irrefutable axiom that humans act purposefully. It is a bit like saying Darwin “discovered” the Theory of Evolution, when what he actually did was articulate it and find very plausible data sets to help explain it to the sceptical mind. Evolution was always there.

For all positivist science, it seems to rely on the very negative contention that the existing state of understanding is correct only because nothing has refuted it. This does not mean that what the laws that science rest on may well be truthful, full stop and unqualified. If Euclidiangeometry is tautological, as a positivist would argue, it can tell us nothing useful about the world we experience. For example, in engineering, the laws of Euclidian Geometry applied to construction. The fact that you would not want to knowingly walk on a bridge notconstructed within the confines of the laws of Euclidian geometry, as it would fall down, implies that these laws have a great benefit to our understanding of the world and are not mere tautological propositions that can deliver up no knowledge capable of being acted upon. Likewise, the Laws that govern how this paper has been written on a computer, or transmitted via the internet to someone-else will not be capable of disproving and are therefore un-scientific, they are right otherwise this would never be written and transmitted.

My contention is that God exists a-priori and that Dawkins in his dismissal of the cosmological argument of Aquinas in particular, shows his lack of understanding of that argument and the distinction between a-priori and a-posteriori knowledge.

Dawkins summarizes (page 77) three of the “five proofs” of Aquinas as “all involve an infinite regress — the answer to a question raises a prior question, and so on ad infinitum.” In his own words, he proceeds to list the three as follows;

- The Unmoved Mover. Nothing moves without a prior mover. This leads to a regress, from which the only escape is God. Something had to make the first move, and that something we call God.

- The Uncaused Cause. Nothing is caused by itself. Every effect has a prior cause, and again we are pushed back into regress. This has to be terminated by a first cause, which we call God.

- The Cosmological Argument. There must have been a time when no physical thingexisted. But, since physical things exist now, there must have been something non-physical to bring them into existence, and that something we call God.

He continues: “All three of these arguments rely upon the idea of a regress and invoke God to terminate it. They make the entirely unwarranted assumption that God himself is immune to the regress. Even if we allow the dubious luxury of arbitrarily conjuring up a terminator to an infinite regress and giving it a name, simply because we need one, there is absolutely no reason to endow that terminator with any of the properties normally ascribed to God.”

So to Dawkins, it is an “unwarranted assumption that God himself is immune to the regress.” He does not say why. Why, Richard, is it unwarranted? If it is so self-evident (and needs no further explanation to his readers) that this is unwarranted, why is it not stated? I suspect it is because Dawkins does not know.

In the physical universe no physical property is infinite. If this was the case, only it would exist. It does not, as you and certainly I exists along with countless other physical things. So how did we come into existence?

The Unmoved Mover of Aristotle (introduced to us specifically in his Metaphysics Book VI, X1, XII and in Physics, Book VII and VIII) comes into play here. The human mind cannot conceive of anything physical without postulating another physical cause for that thing. Cause and effect are a category of the human mind: absent it, and you have no humanmind. All material things have cause and effect; one physical thing bounds another physical thing with nothing being infinite. If nothing is infinite, there simply must be a first cause. Therefore logic clearly dictates that the first cause, if it cannot be physical or material, must be immaterial. We call this God.

Unless you are prepared to boot out Logic as a valid system for ascertaining truth, then you cannot escape the undeniable existence of God.

Perhaps Anthony Flew, whom Dawkins questioned in his book, realised this line of logic when he converted to a belief in a Deity.

An article Dawkins sites in The God Delusion says the following (from Free Inquiry magazine, Volume 25, Number 2):

Flew’s Flawed Science by Victor J. Stenger

“Fortunately, we can avoid an infinite regress. We can just stop at the world. There is no reason why the physical universe cannot be it’s own first cause. As we know from both everyday experience and sophisticated scientific observations, complex systems develop from simpler systems all the time in nature — with not even low intelligence required. A mist of water vapor can freeze into a snowflake. Winds can carve out great cathedrals in rock. Brontosaurs can evolve from bacteria.

And our relatively complex universe could have arisen out of the entity that is the simplest and most mindless of all — the void.”

I cannot see how Stenger avoids an infinite regress. The void then becomes the causeless cause, the prime mover or indeed God. Out of the causeless void comes the universe. I cannot throw out the category of my mind that only allows me to understand, or see the world in terms of cause and effect. Like Aristotle, I cannot throw out or suspend logic on this point. I may have reasoned illogically but am certainly unaware of the error. I may have misread Aristotle, but again, cannot see why.

In The Ancestor’s Tale by Dawkins (page 467–468), he says, “Heredity began as a lucky initiation of an autocatalytic, or otherwise self-regenerating, process. It immediately took off and spread like a fire, eventually leading to natural selection – and all that was to follow.”

So for Dawkins, the initial replicator that kicks it all off is self-causing. I postulate, like Aristotle, that this line of reasoning does not conform to the laws of logic and must therefore be discarded. God (immaterial and unmovable) is the initial cause. What its purpose is is indeed another argument. Applying the method of the physical sciences will not answer the question “is God a delusion?” Only logic will answer that and it is purely a cognitive processof logical deduction.

The science of Dawkins is truly wonderful to read. He is a great teacher who unravels some of the beautiful mysteries of the world. For that I thank him. On God, I would advise him to look at the logic of Aristotle and try to refute it.

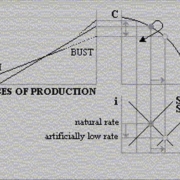

By simply monitoring the deviation from the quarterly trend, we can see over the many years we have been collecting data, that broadly speaking, if a currency pair is trading 5% beyond its quarterly trend line, a relatively quick re-balancing correction generally takes place. What is more, this usually comes in three spikes, one up and two down.

The one up is the market testing the limits on the up phase, the two down is when the initial correction happens, traders can not believe it, they push back up, then the market goes back down and the market starts the correction process. Purchasing power parity matters here and can be very useful in providing indications as to which currencies at any point in time are overvalued re other ones.

The underlying trend itself, as opposed to over-extensions beyond trend, is determined by the ongoing relative balance of the two monies in question, ie., a slow upward* moving Quarterly trend is the result of one money supply expanding faster than the other over and above changes in demand.

Two potential financial products come out of this. Product 1, a strongest currency fund can be developed off the back of this understanding. For any company who trades in multiple currencies and runs cash surpluses, Product 2, a cash overlay service, applying this methodology, for the treasury departments of companies could always mean that the company remains exposed to the strongest currency only.

Suffice it to say, if you know what the real physical money supply is, you can see how the various central banks around the world, intervene via the sale and purchase of bonds in turn supporting certain interest rate policies. The interest rate then has a direct and predictable effect on the determination of the exchange rate on the demand side. This is shown in the following two graphs.

By simply monitoring the deviation from the quarterly trend, we can see over the many years we have been collecting data, that broadly speaking, if a currency pair is trading 5% beyond its quarterly trend line, a relatively quick re-balancing correction generally takes place. What is more, this usually comes in three spikes, one up and two down.

The one up is the market testing the limits on the up phase, the two down is when the initial correction happens, traders can not believe it, they push back up, then the market goes back down and the market starts the correction process. Purchasing power parity matters here and can be very useful in providing indications as to which currencies at any point in time are overvalued re other ones.

The underlying trend itself, as opposed to over-extensions beyond trend, is determined by the ongoing relative balance of the two monies in question, ie., a slow upward* moving Quarterly trend is the result of one money supply expanding faster than the other over and above changes in demand.

Two potential financial products come out of this. Product 1, a strongest currency fund can be developed off the back of this understanding. For any company who trades in multiple currencies and runs cash surpluses, Product 2, a cash overlay service, applying this methodology, for the treasury departments of companies could always mean that the company remains exposed to the strongest currency only.

Suffice it to say, if you know what the real physical money supply is, you can see how the various central banks around the world, intervene via the sale and purchase of bonds in turn supporting certain interest rate policies. The interest rate then has a direct and predictable effect on the determination of the exchange rate on the demand side. This is shown in the following two graphs.

The Leading Composite Monetary Index that we have created incorporates among other things the percentage interest rate carry of one currency over another, in this example, the Euro over the Dollar. Actual Austrian Money Supply shows how a monetary disturbance is required to effect an interest rate change: a tightening of your monetary policy v that of another central bank will cause interest rates to go up in your jurisdiction vis a vis the other jurisdiction. Traders will exploit this arbitrage opportunity. Take notes on points A-E on the graph and then see how these points manifest themselves on the Euro Dollar exchange rate shown next.

The Leading Composite Monetary Index that we have created incorporates among other things the percentage interest rate carry of one currency over another, in this example, the Euro over the Dollar. Actual Austrian Money Supply shows how a monetary disturbance is required to effect an interest rate change: a tightening of your monetary policy v that of another central bank will cause interest rates to go up in your jurisdiction vis a vis the other jurisdiction. Traders will exploit this arbitrage opportunity. Take notes on points A-E on the graph and then see how these points manifest themselves on the Euro Dollar exchange rate shown next.

Hopefully you can get the picture as to how powerful this methodology can be regarding the prediction of medium-long term general exchange rate movements.

The Moving Time Dimension

Mainstream methodologies insist on placing a time dimension on the cause and effect in any given economic situation, so if X takes place then Y will take place with a time lag of A number of months. The Austrian School holds that it is unachievable to regulate actions that are determined by human choice preferences into a fail-safe mathematical model. You can see on the two graphs that points A and B both happen within the same time frame, then point C on the second graph happens some 18 months later.

The point is that although the cause and effect of an increase in Austrian Money Supply and the associated effect on its purchasing power parity is certain, when it will happen depends on the subjective valuations of people. So we apply no mathematical tools to help us predict when the effect will be seen, we trade the position as and when it becomes apparent visually.

To conclude, there is a role for an Austrian Hedge Fund that applies our methodology to exchange rate determination and indeed to credit spreads.

Hopefully you can get the picture as to how powerful this methodology can be regarding the prediction of medium-long term general exchange rate movements.

The Moving Time Dimension

Mainstream methodologies insist on placing a time dimension on the cause and effect in any given economic situation, so if X takes place then Y will take place with a time lag of A number of months. The Austrian School holds that it is unachievable to regulate actions that are determined by human choice preferences into a fail-safe mathematical model. You can see on the two graphs that points A and B both happen within the same time frame, then point C on the second graph happens some 18 months later.

The point is that although the cause and effect of an increase in Austrian Money Supply and the associated effect on its purchasing power parity is certain, when it will happen depends on the subjective valuations of people. So we apply no mathematical tools to help us predict when the effect will be seen, we trade the position as and when it becomes apparent visually.

To conclude, there is a role for an Austrian Hedge Fund that applies our methodology to exchange rate determination and indeed to credit spreads.